News | Property Market Updates

UK Property Market Conditions Q1 2026

Allsop Outlook

"It was one of those March days when the sun shines hot and the wind blows cold: when it is summer in the light, and winter in the shade." Charles Dickens Great Expectations

The first quarter of 2026 has been one of surprising extremes, akin to the famously variable British spring weather. Bright spots appeared early, with slowing inflation and the after-effects of the rate cut in December combining to ‘warm up’ the real estate market across all sectors.

However cold winds suddenly appeared in March, blowing away both the first draft of this commentary and the optimism with which the New Year had begun.

There are now far more clouds in our sky than any of us were expecting and the likely after-effects of recent events in the Middle East are set to be profound for the property sector, especially given the fact Britain was already wearing ‘the wrong coat’ for this type of stormy macro-weather! Firstly, the cumulative effect of higher employment costs was already creating a challenging environment for certain sectors:

- Residential landlords employing managing agents, maintenance contractors, and administrative staff were likely to face higher labour costs.

- Developers and construction firms, already navigating viability challenges, were going face increased costs for directly employed workers and subcontractors – the sharp fall in Construction output in January and major housebuilder Berkeley PLC announcing a pause in both hiring and land acquisition, further evidence of the scale of the challenge facing this segment of the market.

- Retailers and hospitality operators occupying commercial property were looking at margin compression, for which the traditional remedy has long been store closures, lease surrenders and headcount reductions; and/or consumer price rises where possible.

Secondly, sluggish economic growth, both historic and projected, had been lurking on our horizon for some time.

- An economy growing at 0% to 1% generally provides weak support for occupier demand across all asset classes: retailers inevitably face weaker consumer spending, office occupiers face more uncertain headcount growth, and residential buyers face both income uncertainty and affordability constraints.

The combination of weak growth, elevated borrowing costs, and rising energy bills was already creating a challenging backdrop for property values, transaction volumes, and development activity well before the Iran conflict broke out. But this storm cloud was at least predictable and a known quantity which markets could prepare for.

Thirdly the labour market data reveals a troubling long-term trend: a significant exodus of British nationals from the UK.

- The ONS's revised migration methodology shows British nationals leaving the UK at an average rate of 92,000 per year between 2021 and 2024 - dramatically higher than the previous estimate of just 6,500 per year under the old methodology. While some of this reflects improved measurement rather than a genuine change in behaviour, the scale of the revision suggests a substantial and sustained outflow of UK citizens.

- Evidence from Companies House reinforces concerns about capital and talent flight among higher-net-worth individuals. Data on company directors shows a marked increase in re-domiciliation abroad, with directors changing registered addresses to overseas jurisdictions at elevated rates through 2024 and 2025.

- Wealth migration consultancies and banks in recent months anecdotally reported record levels of enquiries from UK-based high-net-worth individuals exploring relocation, driven by concerns about tax policy, regulatory burden, and the broader economic and political environment. The direction of some of those enquiries ‘reversed’ as soon as the scale of the Iran-USA/Israel military action became clear in March, with some HNWIs contemplating using the UK as a safe haven, but these enquiries were not at the scale of the sustained outflow we’ve seen in recent years.

An exodus of affluent individuals has direct implications for the prime London residential market, where demand is heavily dependent on internationally mobile high-net-worth buyers and tenants.

At the same time high unemployment (especially youth unemployment), falling job vacancies and negligible real wage growth imply that the engine of the UK economy is running low on fuel. Rental and mortgage affordability concerns, as a well as new cost-of-living crisis, could resurrect themselves as factors late in 2026 and into 2027 if the geopolitical and trade situations persist or worsen.

The implications of the renewed instability in the global financial markets are also now becoming painfully clear: financing costs will - barring a sudden and lasting Middle Eastern peace deal - remain structurally higher, requiring a repricing of yields and investment returns over the rest of 2026.

We have already seen the impact of this, with buyers on transactions in March facing near-overnight increases in their debt costs of ~100bps at best, or at worst, a sudden withdrawal of lender appetite.

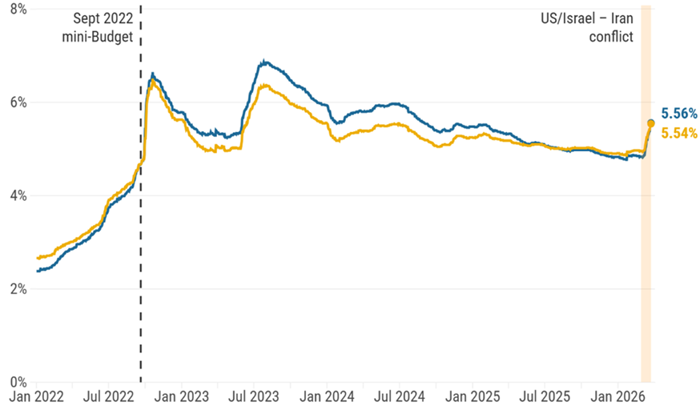

Average 2yr & 5yr mortgage rates - Jan 2022 to Mar 2026

Source: Moneyfacts ¦ as at 25th March 2026 Source URL

In the domestic mortgage market, we’ve seen a similar phenomenon play out, albeit at a larger scale.

- Analysts Moneyfacts estimate that lenders withdrew more than 1,500 mortgage products in the 3 weeks between 9th March and the 25th: equating to roughly a fifth of the overall mortgage market. On one day (the 21st) 448 mortgage deals were withdrawn which is the highest amount in a single day since the aftermath of the Sept 2022 minibudget.

- First-time buyers have seen the average two-year fixed rate at 95% loan-to-value (LTV) jump back above 6% and more than 200 deals at the 95% LTV tier being withdrawn in March. This added more than £1,000 p.a. to the cost of a £250k loan at 95% LTV in just 3 weeks.

All this will weigh negatively on the new build & apartment markets, reducing the demand pool for housebuilders’ stock & smaller ‘starter’ homes, hurting viability as buyer confidence falls, with builders and conventional vendors having to cut prices or increase the levels of incentives to keep sales rates moving.

"Recent years have seen an unprecedented increase in cost and regulation, at a time of increasing interest rates and faltering consumer confidence, amidst prolonged geopolitical and macro-economic volatility and uncertainty…In the first two months of 2026, we had begun to see signs of a modest recovery in sales volumes. However, recent geopolitical events and the macroeconomic consequences, including reduced potential for further rate cuts, could reduce confidence in a near-term market recovery. This has now become a reality." Berkeley Group Strategy and Trading Update ¦ 1st April 2026 Source URL

The energy price shock now working its way through the system will now add materially to consumer price inflation through Q2 and Q3 2026. The MPC's own March projections projected CPI to approximately 3.5% in Q3 2026, with energy increases contributing ~0.75 percentage points. Although I suspect that forecast will be revised upwards once the scale of the damage and disruption to petrochemical infrastructure, and trade, becomes fully clear.

Private sector inflation estimates have already adjusted above the BoE’s number: Experian's full-year 2026 inflation forecast is now 4.3% thanks to rising fuel prices and the July energy cap reset. Household inflation expectations also jumped to 5.4% in March from 3.3% in February, raising the spectre of a wage-price spiral as both public & private sector workers seek higher pay settlements to offset the increase in CPI.

The worry, from a monetary policy perspective, is that the ~2month lag in the ONS CPI means that the Bank won’t be working with ‘live data’ that is reflecting higher input prices as a result of the closure of the Strait of Hormuz, until the MPC meet on 18th June at the earliest (they don’t meet in May) or on 30th July at worst.

By late July, the new OFGEM price cap plus price rises caused by Hormuz-linked supply shortages AND employers’ responses to April’s increases in employment costs will likely be feeding through to the ONS consumer price data. And that pass through might be rapid and involve a large upward ‘jump’ that could nudge the MPC into a Summer rate rise. We could also be using the word Stagflation a lot more by then.

I hope not of course, but who knows at this point!?

Fundamentally we have just seen a shift in financing conditions faster than at any point since 2008, but further clouds are below the horizon racing towards us.

This is not yet a crisis, but the margins for error (and profit) have narrowed dramatically and suddenly across all sectors.

The only forecast I can confidently offer at the end of March is that conditions look set to be highly variable - mostly cloudy and showery with only isolated sunny intervals - for the foreseeable future.

The Hormuz Situation - Possible Scenarios

On 28 February 2026, US-Israeli Operation Epic Fury struck Iran, killing Supreme Leader Ayatollah Khamenei. Iran retaliated by effectively closing the Strait of Hormuz from 2 March, something it had threatened for 45 years but never previously achieved.

The Strait carries approximately:

- 20% of global oil supply (~20 million barrels/day)

- 22% of global LNG exports

- Roughly one third of the world's seaborne fertiliser trade

- Roughly one third of the world's helium supply (critical for semiconductor production)

- Approx. 11% of total maritime trade volume

There appears to be broadly two scenarios that could now play out, as of the end of March 2026

Use of Artificial Intelligence

This document includes augmented content with the assistance of an AI tool, under the supervision of the Allsop Research team. All content has been reviewed and approved by Seb Verity, Head of Research.

Related Insights

Allsop May Property Market Update

Our May 2026 Market Update is now live - covering the economic overview, the impact of the Middle East conflict on UK proper...

Allsop Property Market Update December 2025

If you would like some advice about your property from any of our teams, complete our contact form with your details of your ...

What does the Autumn Budget mean for the property sector?

Phew... or Too Few? As Chancellor Rachel Reeves stood up at the despatch box and delivered the Budget in person, rather than ...

Allsop lifts the trophy for Commercial Agency of the Year at PROPS Awards

The PROPS Awards, recognises and celebrates individuals and companies that have excelled in the property sector while raising...